Alipay

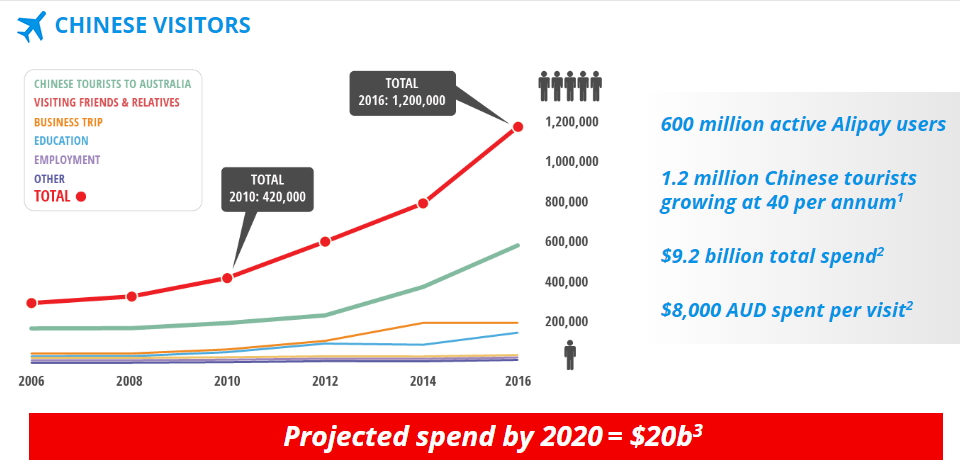

China is now Australia’s fastest-growing, largest and most valuable tourism market. Growth rates have been incredible, and they now have about 30% of total spend by international visitors in Australia.

Added to that the number of Chinese resident and students in Australia is steadily growing, now about 30% of international students in Australia come from China.

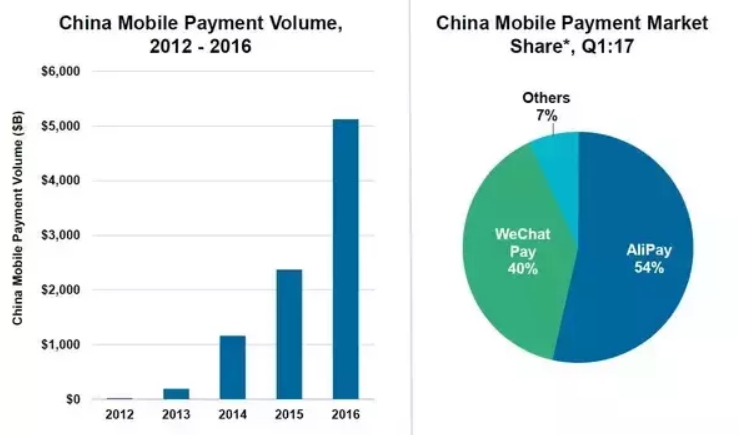

Itwire studies have shown that 99% of Chinese tourists in Australia have Alipay. In 2018, Alipay transaction volume in Australia increased by 110% and using Alipay the amount spent per person was up by 40% and its a wide range of products that they buy here.

This is opening up a terrific market in Australia for Alipay.

If you have any serious interest in getting your share of this market, I do suggest that you consider adding it as a payment type in your shop.

So we are pleased that we are offering a direct integration. It will work through Tyro EFTPOS which as Tyro has no contracts, so it is easy for any of our clients to add this payment type if they want it. If you are interested, let me know.