The government has announced plans to ban debit card transaction fees, potentially starting January 1, 2026. This proposed ban, however, doesn't extend to credit card transactions.

A Global Trend in Payment Practices

In truth, this banning of debit surcharges was expected. Many countries, including the European Union and China, have implemented similar bans. Australia is now catching up with this global trend in consumer protection and payment fairness.

The Current Landscape: Widespread Surcharges

Today, many organisations, including government authorities, charge these fees. For instance, the Australian Taxation Office (ATO) imposes surcharges on card payments. This practice is widespread across various sectors and affects consumers daily.

Consumer Frustration: The Hidden Costs of Convenience

Many consumers, myself included, are frustrated with the current situation. It's common to hear complaints. I know I am not the only one who doesn't like that a $7.50 coffee and doughnut is charged at $8.00. If I am told it's $7.50, I get a receipt for $7.50, and in the bank, I see $8.00.

This sentiment is extreme here when the surcharge seems disproportionate to the transaction amount. From my extensive research into bank systems, I can confidently say that the cost of processing a $7.50 debit transaction is nowhere near 50 cents. Taking money from one account and putting it into another cost the bank no more than a few cents.

Potential Impacts on the Retail Scene

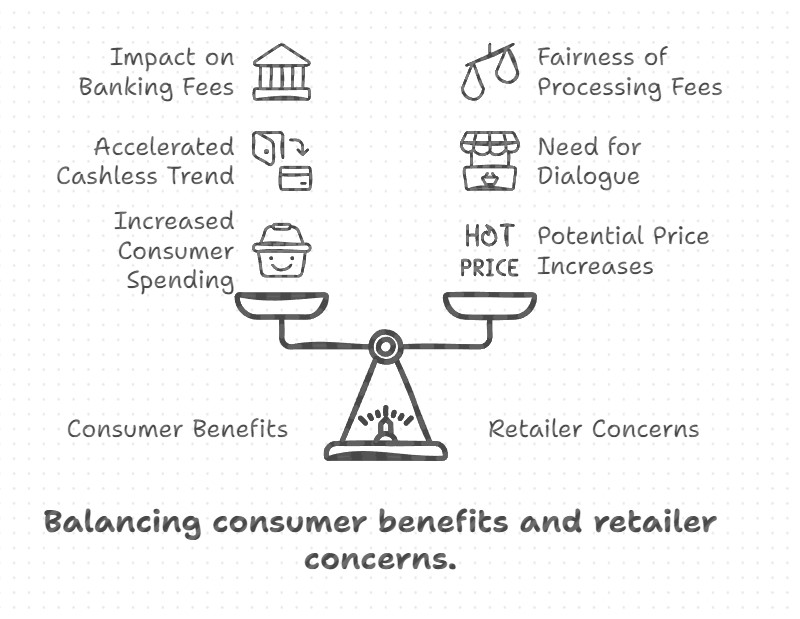

The ban on debit card surcharges will likely have far-reaching effects on retail. Here are some potential economic points to consider:

Increased Consumer Spending

By removing a barrier to debit card use, we might see a slight increase in overall consumer spending. The absence of surcharges could encourage more frequent use of debit cards, potentially leading to more transactions.

Acceleration of Cashless Trend

Australia is rapidly becoming a cashless society, and this ban will accelerate this trend. What is keeping cash going is the lower fees to the consumer. If debit cards become even more cost-effective for consumers, they will use them more.

Potential Price Increases

Some businesses might have to increase their prices depending on how this is implemented. We already have too much inflation that refuses to go away, potentially exacerbating the issue.

Changes in the Banking Sector

Today, these fees play a significant role in banking pricing. If banks are not making money from these fees, what adjustments will they make to their business charges? This is a crucial question that needs addressing.

Retailers' Concerns: Questions That Need Answers

Here are some questions that I think retailers need to ask now while people are talking about these changes, If they miss this opportunity, what you will find is that the banks will talk, consumer groups, government and since retailers are not talking what will come out of it?

-

Costs: Who will pay for these costs if fees are eliminated? Retailers should be concerned about who will absorb these costs if surcharges are banned.

-

Fee discrepancies: There's a noticeable difference in processing fees charged to small businesses compared to large corporations. Why are small businesses often charged up to twice as much? The costs surely are not that much more!

-

Premium Card Fees: Retailers are often charged higher processing fees so the bank customers can get benefits like Qantas points. Is this justifiable?

-

Card-Specific Surcharges: Retailers cannot charge different surcharges for different types of cards. The ACCC is wrong to make it mandatory to charge the same fee for a standard Visa card and a premium Visa card.

-

Bank Fees: Why are our debit and credit card fees so much higher than those of many European countries and China? This deserves a thorough investigation.

-

Unfair fees: Unlike large retailers who can negotiate better rates with banks, small businesses often pay double the fees for card processing. Besides being unfair, it means that the effect of these costs will have more impact on them.

Moving Forward: The Need for Dialogue

As we approach the potential implementation date, consumers and businesses must stay informed about these changes. Retailer representatives should engage with the government to address their concerns.

Moreover, this presents an opportunity to review and potentially overhaul Australia's card payment system.

The Future of Payments in Australia

Today, about 12% of transactions are made using cash, down from 27% five years ago. We're rapidly moving towards a cashless society.

Conclusion: A Complex Issue Requiring Careful Consideration

In conclusion, while the proposed ban on debit card surcharges is generally positive for consumers, other stakeholders have legitimate concerns. The government must carefully balance consumer protection with the financial realities retailers face.

Frequently Asked Questions (FAQ)

Q: Are there any exceptions to the debit card surcharge ban for specific industries or transaction types?

A: As of now, I have heard no talk of any exceptions being announced. The government will likely provide more details as the policy is developed.

Q: What measures will be taken to ensure businesses don't increase prices to offset the loss of surcharge revenue?

A: I am guessing here, but I suspect the Australian Competition and Consumer Commission (ACCC) may monitor for unfair price increases.

Q: How will the ban impact digital wallet payments and mobile payment platforms?

A: I am wondering about this. Apple, for example, has a special fee. This is an overseas fee, so it's unclear whether it's covered here. So, we do not know whether this ban applies to all debit card transactions made through digital wallets and mobile platforms.

Q: How will this affect loyalty programs or cashback offers tied to card usage?

A: The ban may affect these programs. I am worried that if the banks face reduced revenue from merchant fees, they might move to a retailer-pay model.

Q: What support or resources will be available to help small businesses adapt to these changes?

A: The government hasn't announced specific support measures yet; retailer associations should investigate.

Q: How might this affect international transactions or tourists using foreign-issued cards in Australia?

A: Who knows? In this situation, the merchant may be charged the fee.

Q: How will this impact the competitiveness of different payment methods in the Australian market?

A: It makes debit cards more competitive compared to credit cards and probably cash.

Many details will need to be developed and implemented.