Here are two reasons why the present card payment system is wrong.

The current card payment system in Australia is fundamentally flawed. It unfairly burdens merchants, particularly on small businesses. While convenient for consumers, this system has created a cost crisis that threatens the viability of many Australian retailers.

The Card Payment Boom

The increase in card payments has been remarkable, but it has also placed significant financial burdens on merchants as I will show.

The Cost of Convenience

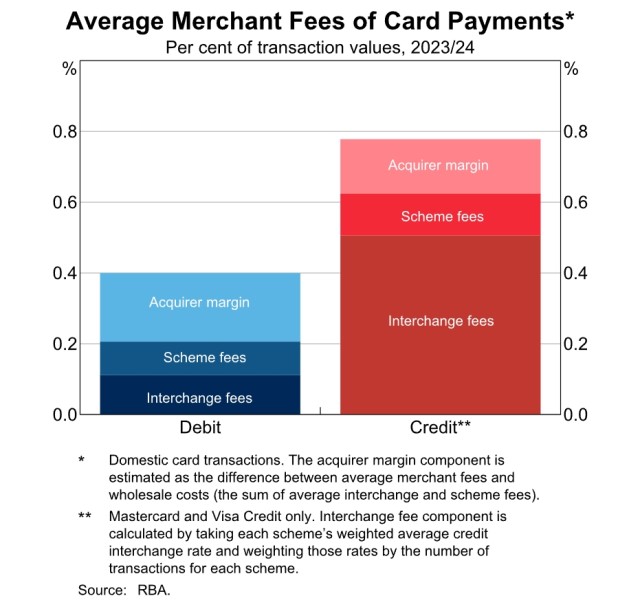

Merchants bear a significant portion of the costs associated with card transactions:

- 50% of fees on debit card transactions

- 80% of fees on credit card transactions

These costs are mainly in the interchange fees, which make up about 80% of merchants' total fees for card transactions.

Understanding Interchange Fees

Interchange fees serve several purposes:

- Transaction processing: Covering the costs of handling electronic payments

- Risk management: Mitigating fraud and credit risks

- Network maintenance: Supporting the infrastructure that enables card payments

Although the fees have dropped over time, as card usage has increased, total card costs have skyrocketed.

My first thought is why the fees here are so much higher than in many European countries. Indeed, Australia, with its lower cost structure, should be cheaper.

I don't accept the bank's argument that our costs must be higher because of our low population. Australia's population is higher than most European countries.

In 2021, the average merchant service fee in Australia was 0.9%. In the EU, the average fee is 0.3% for credit cards and 0.2% for debit cards.

The Effect on Retailers and Consumers

The current fee structure creates a complex dynamic, as retailers pay most fees.

Now, card issuers offer more attractive terms to cardholders to attract more business, such as rewards points, which the card issuer charges the retailer. Is it correct that retailers should be charged these reward costs? I do not think so. Plus, under the current system imposed by the ACCC, retailers cannot surcharge many of these reward systems. For example, a premium VISA card must be charged the same surcharge as a standard VISA card.

Cost of card payments

Although the costs are dropping, as card usage has exploded, the total cost has skyrocketed. The immediate problem with these fees, which are dropping, is that they are still high in Australia compared to other countries like Europe. If in Europe, with its higher cost structures, it can be cheaper, why not here?

Over the same period, we have seen that card suppliers have moved the cost they levy from the customer to the merchants. Today, merchants pay almost all these costs.

The Reserve Bank of Australia has written a good article on the cost of Card Payments. You can read it here.

It is unfair that Small Businesses Pay More

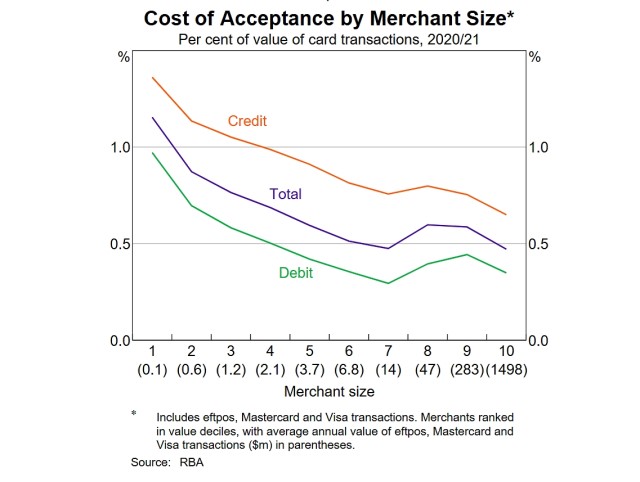

A study by the RBA found that, on average, small merchants pay transaction fees that are about three times higher than those paid by large merchants. This significant gap raises questions about fairness and produces major competitiveness problems.

Factors Behind Higher Fees for Small Businesses

Several factors contribute to the higher costs faced by smaller merchants:

-

Limited Bargaining Power: Large businesses can better negotiate favourable wholesale fees for processing card transactions.

-

Fixed Costs: Accepting card payments involves fixed costs like purchasing or renting payment terminals. For smaller merchants, these costs are spread over a lower volume of transactions, leading to higher average costs.

-

Pricing Plans: I often see smaller merchants opting for short-term plans, which are generally more expensive in the long run.

-

Lack of Volume Discounts: Larger merchants benefit from volume discounts due to their higher transaction volumes, a benefit that's out of reach for most small businesses.

The Numbers Tell the Story

The disparity in costs is significant:

- The smaller merchants on the chart have an average cost of acceptance across all card types of 1.15% of transaction values.

- In contrast, the largest has an average cost of acceptance of just 0.47%.

The Broader Impact

This cost disparity has several implications:

-

Reduced Competitiveness: Higher transaction costs make it harder for smaller retailers to compete with larger retailers.

-

Cash Preference: Some small merchants discourage card use or implement minimum purchase amounts for card transactions, inconveniencing customers.

Here is a good article on the problems of small vs large retailers here.

Looking Ahead: Technology potential solutions.

Digital Wallet Integration:

Improvements to digital wallets like Apple Pay, Samsung Pay and Google Pay in the Australian card payment ecosystem could bypass some traditional card network fees, providing a direct, less costly payment route. These could bypass the card entirely.

Bitcoin as a Potential Solution

Items like Bitcoin present an intriguing alternative to Australia's current card payment systems, particularly for small businesses facing high transaction fees. Bitcoin has much lower transaction costs as it has no interchange or bank fees, plus it offers a level of anonymity and security that cash provides.

What the government should do?

-We should introduce a low-cost card payment system with the same fee, regardless of the business's size. We have one now, called cash, but we need something to replace it. Merchant surcharging should not be allowed in that payment system.

-Transparency in fee structures. We cannot act until we know exactly what is happening.

-A review of the current costs of interchange fees. Why do the card providers need so much in fees?

-A review of the card costs: Why should merchants have to pay for the reward system for many cards? If card suppliers want to market their cards more, they should pay for it. The current surcharge rules by the ACCC are wrong, as they do not allow a merchant to charge a surcharge on many premium cards.

Conclusion

The Australian payment system needs urgent reform to protect small businesses and ensure fair competition. The convenience of card payments shouldn't come at the expense of our vibrant small business sector.