Stock Shrinkage from Stocktake to Action

You already spend time and money counting the stock in your shop. Let's take a look at the real story behind your missing stock. I will show you how to calculate stock shrinkage and identify causes using your Point of Sale (POS) system. What we want is better control of profits.

Key Takeaways

- Stock shrinkage value is the dollar difference between theoretical stock value and your actual stock you count.

- Shrinkage rate is generally calculated by the stock shrinkage divided by book stock value.

- Shrinkage is divided up into known values such as damage, expiry, and write-offs, while unknown shrinkage is the unexplained difference left over.

- External shrinkage includes shoplifting and supplier shortages, and internal shrinkage includes process errors, incorrect pricing and staff actions.

- Knowing the causes can help you do something about it.

What Is Stock Shrinkage?

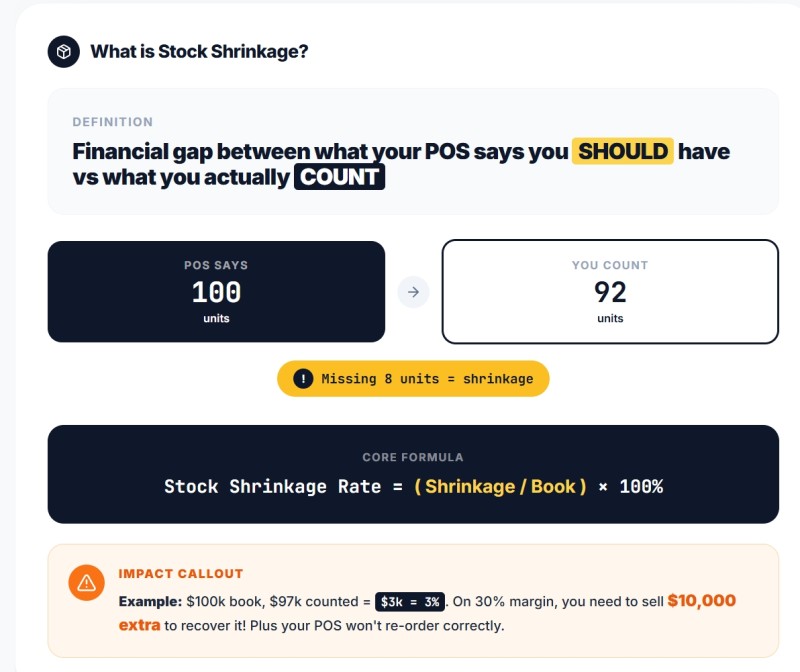

Stock shrinkage is the difference between the stock value recorded in your system and the value you actually count on your shelves. It is the financial gap between what you should have and what you do have. For example, if your POS says you should have 100 units of a stock line, but your physical count finds only 92, the missing eight units are your stock shrinkage.

Since we have so many lines, the only useful ratio is the dollar value, so we measure:

So, for example, if you should have $100,000 at cost and your count finds $97,000, the $3,000 difference is your stock variance, which is $3,000 / $100,000 × 100% = 3%. In this example, on a 30 per cent gross margin, you need to sell $10,000 worth of extra goods to get back to where you should have been.

It also distorts your buying decisions, since the computer thinks you have more stock than you should have; it does not order enough. Over time, you will not trust your stock figures as that 3% adds up.

Let us Calculate Your Stock Shrinkage Rate?

Here is an easy two-step process:

Step 1: Calculate the stock shrinkage value

- Book stock value: your POS reports before the stocktake have the book value. If your system, unlike our POS system, cannot give you this value, your accountant can tell you the figure. It's actually a fairly easy figure to calculate.

Now the Physical stock value is what your POS System said after the stocktake.

Step 2: Calculate the shrinkage rate

Simple Example:

- Book stock at cost: $100,000

- Physically counted stock at cost: $97,000

- Stock shrinkage value (variance): $3,000

- Shrinkage rate: $3,000 ÷ $100,000 × 100 = 3%

The business has identified a $3,000 stock variance. Now, further investigation is required to determine how much is attributable to theft, damage, receiving errors, unrecorded returns, or other causes.

What Does Stock Shrinkage Include?

Stock shrinkage includes a wide range of causes. You need to separate them. Generally, most retailers divide them into two main categories: external shrinkage and internal shrinkage.

External Shrinkage Examples

- Shoplifting and opportunistic theft

- Organised theft or "grab and run" incidents

- Fraudulent or abusive returns

- Supplier shortages or under-deliveries

Internal / Process Shrinkage Examples

- Employee theft or unauthorised discounts

- Receiving errors and incorrect quantities on deliveries

- Wrong pricing and barcode mistakes

- Incorrect stock adjustments in the POS

- Unrecorded damage or expired stock

- Misplaced goods within the store or back room

- Unprocessed or partially processed customer returns

I find it helpful to separate known shrinkage from unknown shrinkage. Known shrinkage includes stock you have already written off in the system for damage, breakage, expiry or other approved reasons. Unknown shrinkage is the unexplained difference between your POS records and the physical count after accounting for all known movements.

For example, if your variance is $3,000 and you can see $1,200 of recorded damage and $300 of recorded expiry, the remaining $1,500 is your unknown shrinkage.

The more information you know, the better. For example, if staff leave damaged greeting cards in a drawer instead of recording them, they become unexplained shrinkage. When, in fact, they are a known problem. It should never have happened.

Departments

What I find very useful is to redo the calculation by department.

Generally, we find different departments have different problems.

Conclusion: Make Your Stocktake Work for You

Stock shrinkage is not just a number you give your accountant at the end of the year. Stock shrinkage is a powerful signal that your stock control, receiving, pricing or security needs attention. When you separate known and unknown shrinkage, recognise the special risks in newsagency departments, build a simple control framework and use your POS system to investigate.

Written by:

Bernard Zimmermann is the founding director of POS Solutions, a leading point-of-sale system company with 45 years of industry experience, now retired and seeking new opportunities. He consults with various organisations, from small businesses to large retailers and government institutions. Bernard is passionate about helping companies optimise their operations through innovative POS technology and enabling seamless customer experiences through effective software solutions.